When the West Asia conflict erupted on 28 February, the impact was felt in Nepal within weeks. Over a third of the country's tourism businesses reported revenue losses exceeding more than four years of average wages.

The conflict affected long-haul flights, disrupted the air corridors and increased the price of aviation fuel. With only brief and fragile ceasefires, the structural consequences are becoming clearer: this is not a temporary disruption but a sustained threat to one of Nepal's tourism sector that employs over 1 million people.

These are jobs across a wide range of sub-industries: hotels, trekking and expedition companies, travel agencies, guiding services, and the dense network of local businesses that depend on visitor spending, particularly in rural and remote communities.

For many of these businesses, especially those in high-altitude trekking corridors, the March–May spring season is not merely peak season, it is the primary revenue window for the rest of the year. A sustained contraction in arrivals during this period carries livelihood consequences that extend far beyond balance sheets.

The mechanisms of impact are multiple and reinforcing. The blockage of the Strait of Hormuz has disrupted global oil supply chains, with downstream consequences for Nepal given its dependence on fuel imported routed through India.

Rising fuel costs have elevated airfares, reduced demand for long-haul travel, and constrained rerouting options that airlines and operators would ordinarily deploy. The result is a sector facing simultaneous demand suppression and connectivity failure.

Governance Lab conducted a rapid industry pulse survey between 25 March- 3 April, drawing 42 responses from tour operators (38%), trekking and expedition companies (29%), hotels and resorts (17%), travel agencies (10%), and guides or freelancers (5%).

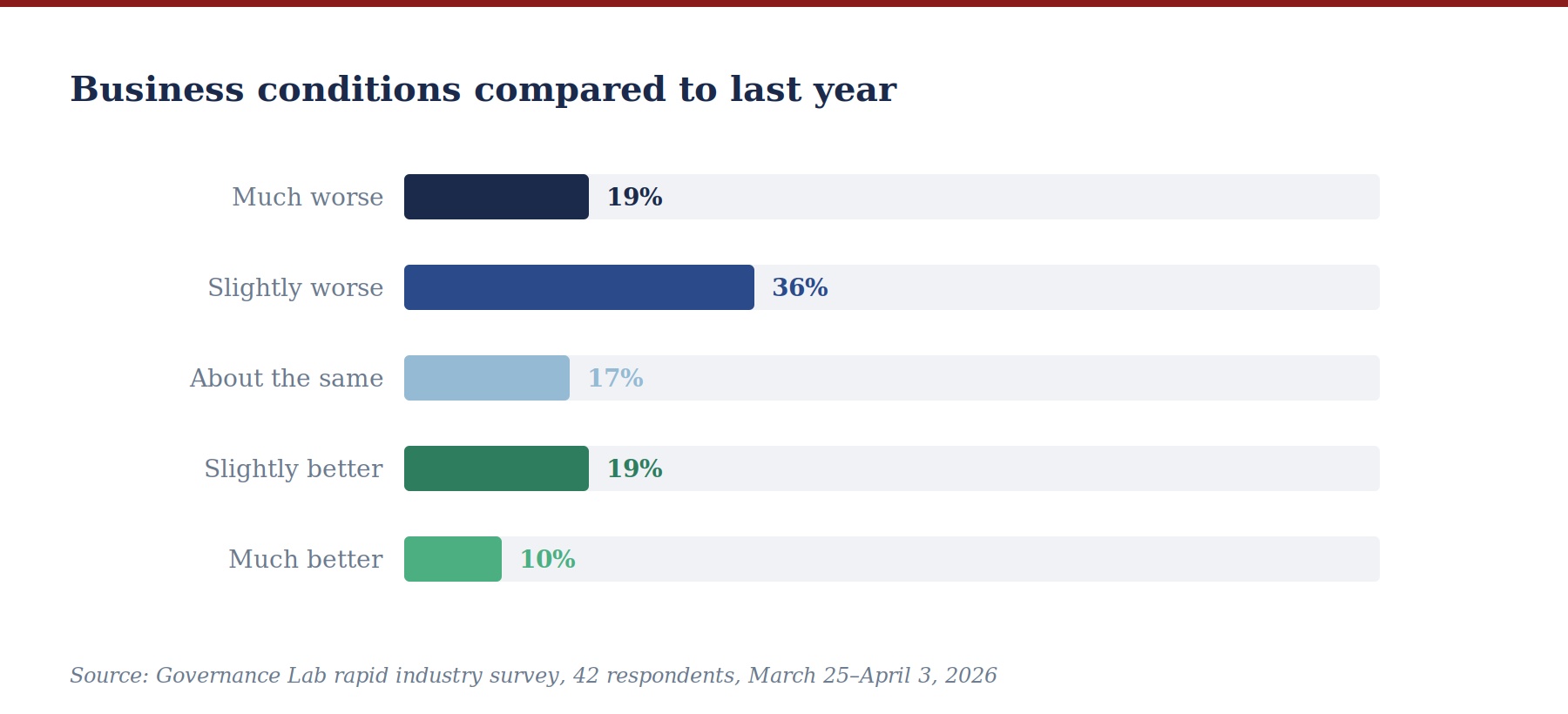

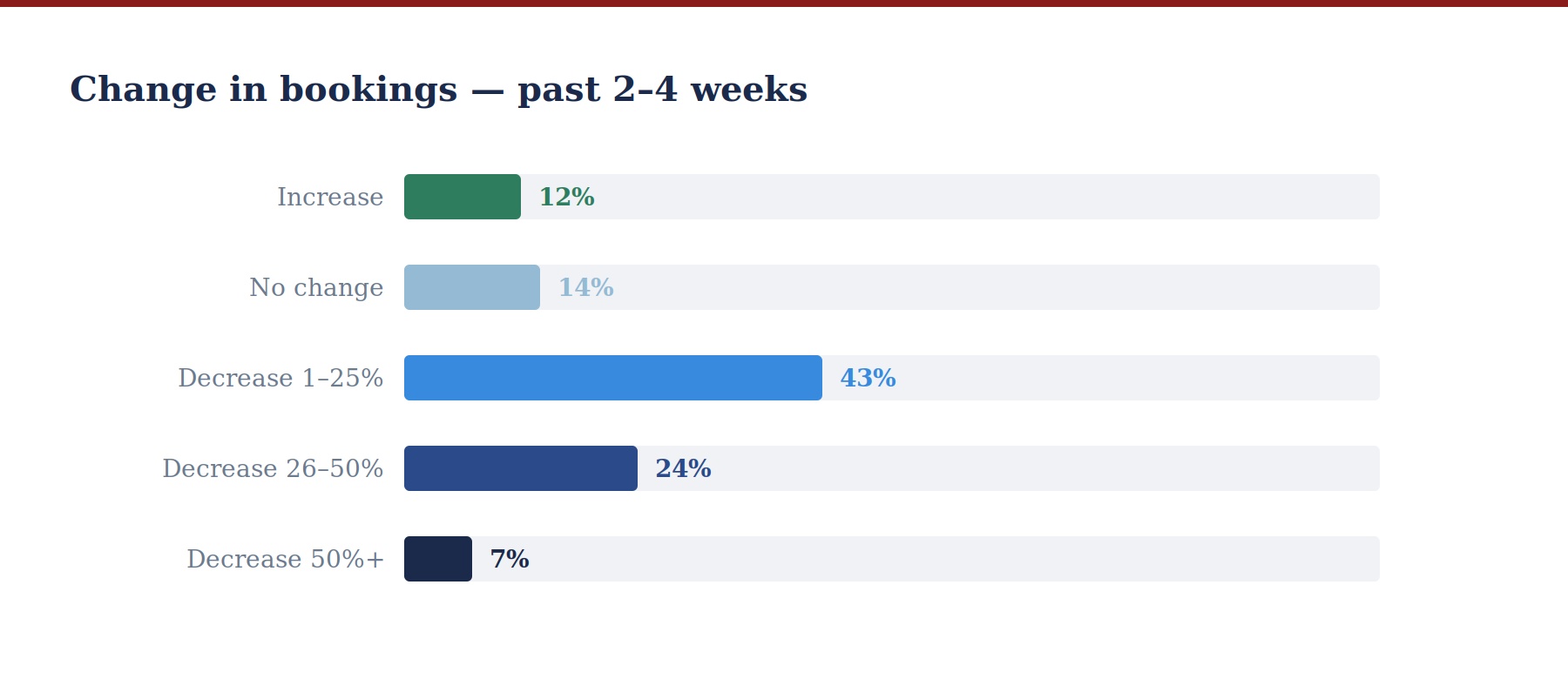

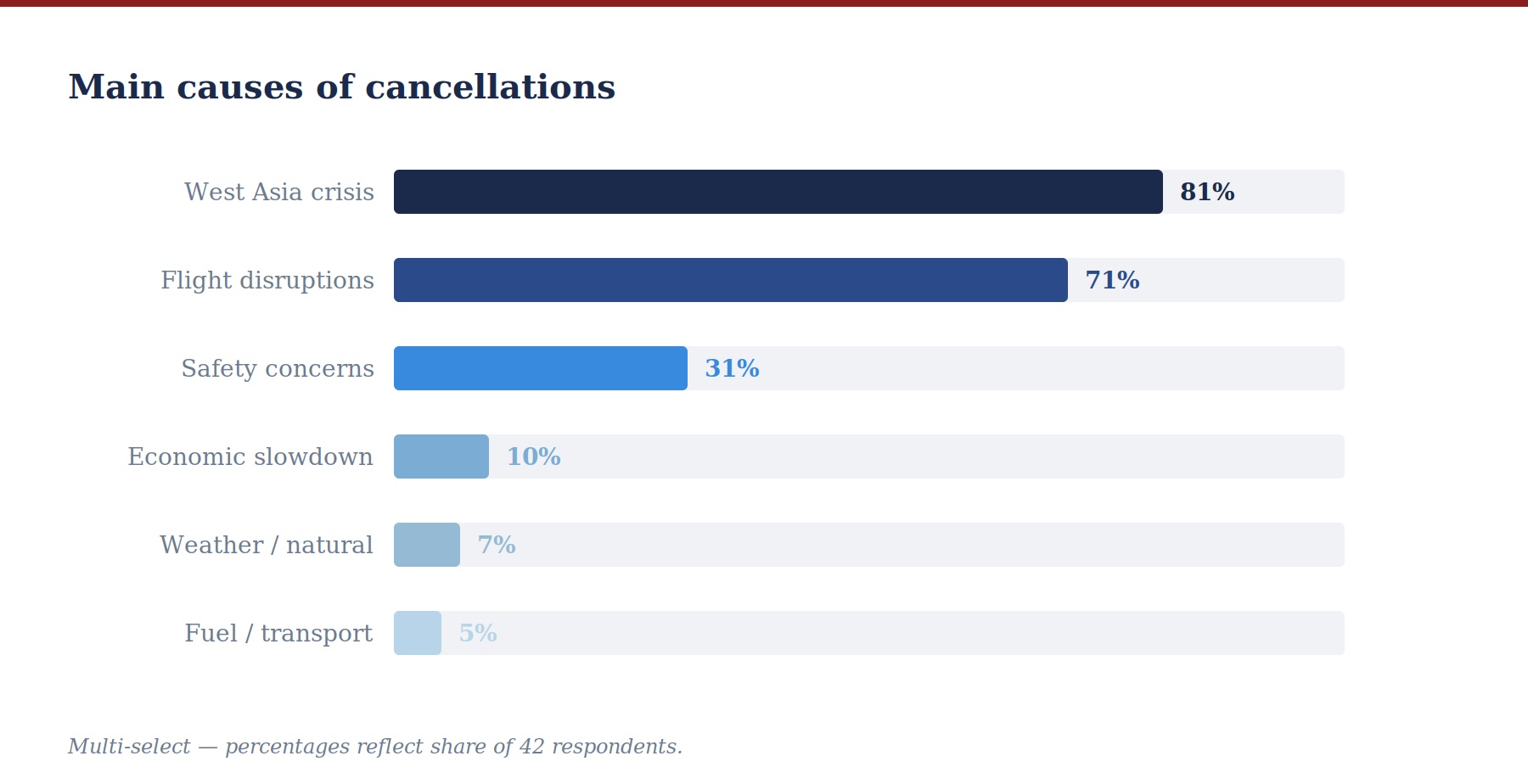

Fifty-five percent of respondents described current business conditions as worse than the same period last year, with 19% characterising it as ‘much worse’. Seventy-four percent reported a decrease in bookings over the prior two to four weeks. On causes: 81% attributed cancellations primarily to the West Asia conflict, 71% to flight disruptions, and a further cohort to safety concerns.

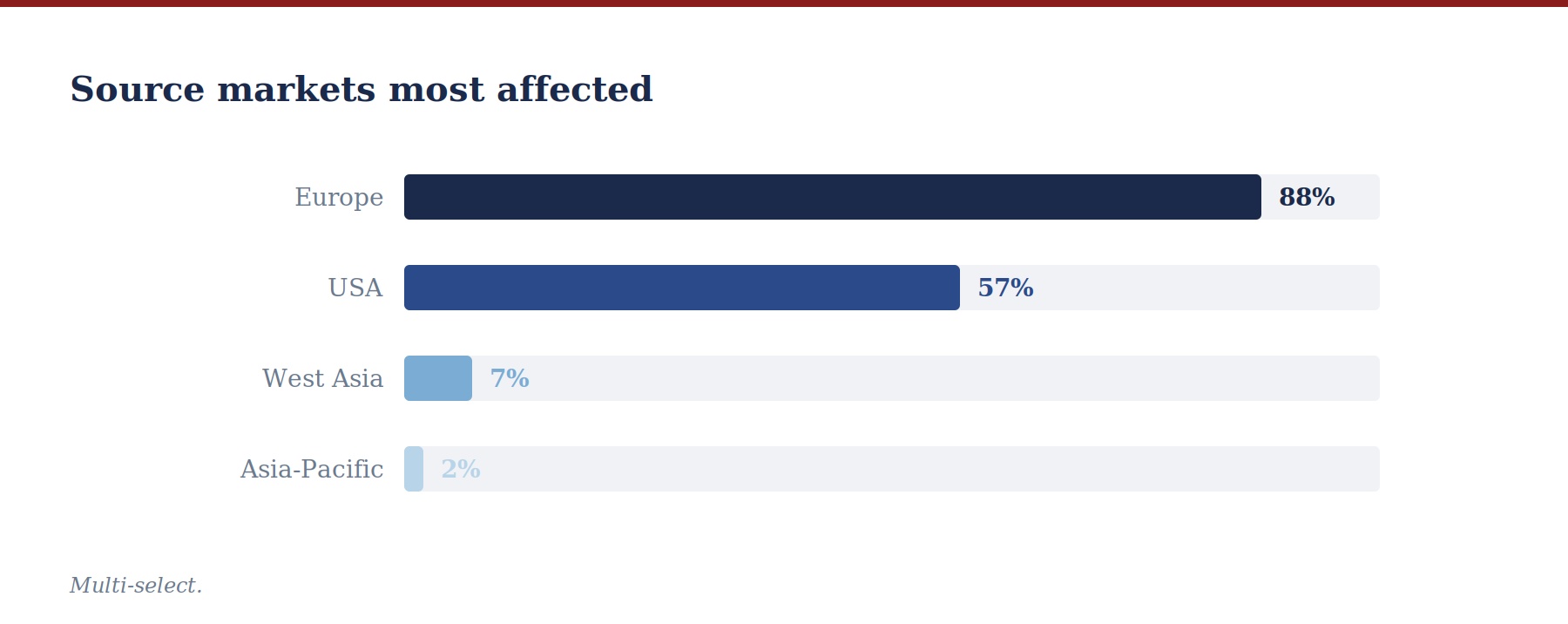

Eighty-eight percent of respondents identified Europe as the most affected source market; 57% identified the USA. These represent the highest-value, longest-staying visitor segments in Nepal's inbound tourism profile. European arrivals in March 2026 fell to 20,876, down from 25,742 in March 2025, a 19% year-on-year decline.

Arrivals from the Americas dropped from 13,907 to 10,374 over the same period. West Asia recorded 1,718 arrivals against 2,732 the previous year, a 37% contraction.

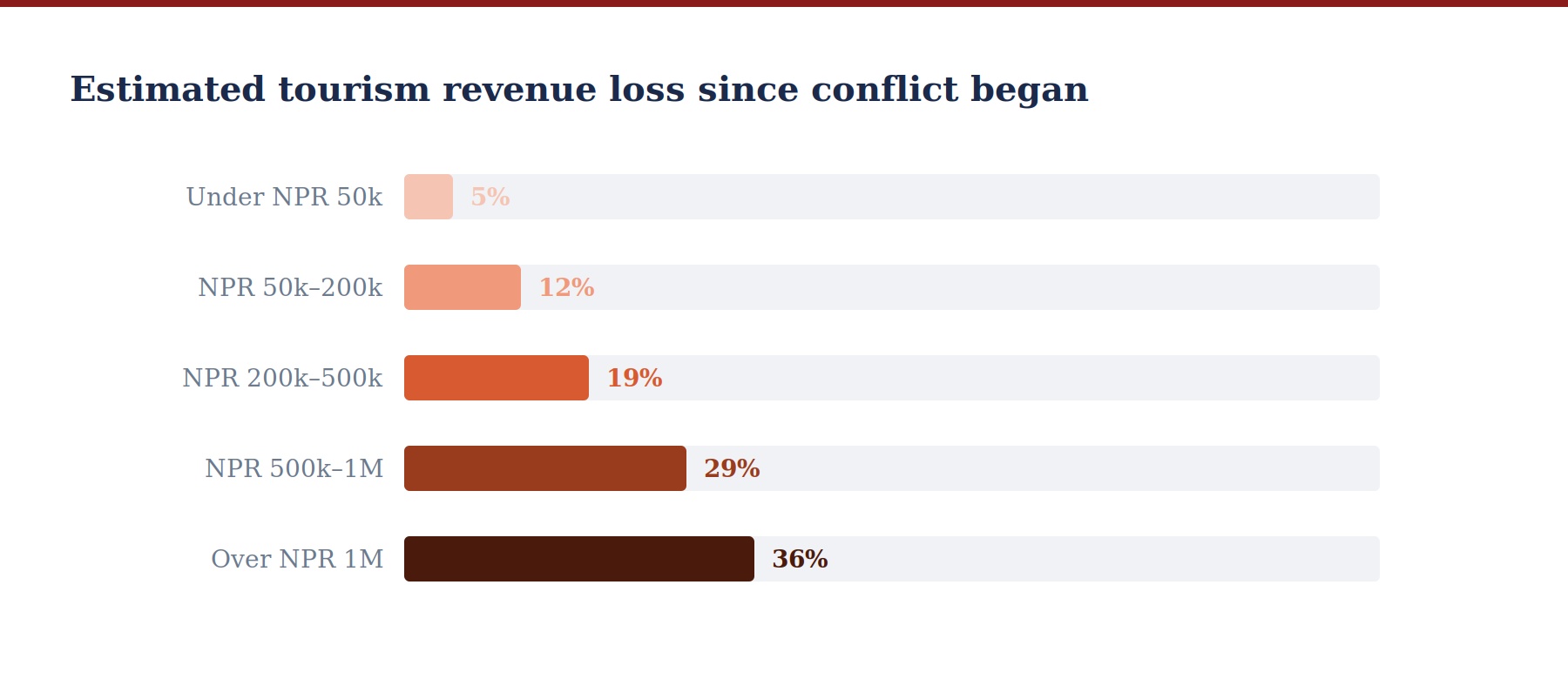

Financial damage is already significant and unevenly distributed. Thirty-five percent of respondents reported revenue losses exceeding Rs1,000,000 since the conflict began; 29% reported losses between Rs500,000-Rs1,000,000. The average monthly salary in Nepal is Rs19,800, meaning the losses reported by the most affected operators represent years of average earnings, concentrated into a period of just over two months.

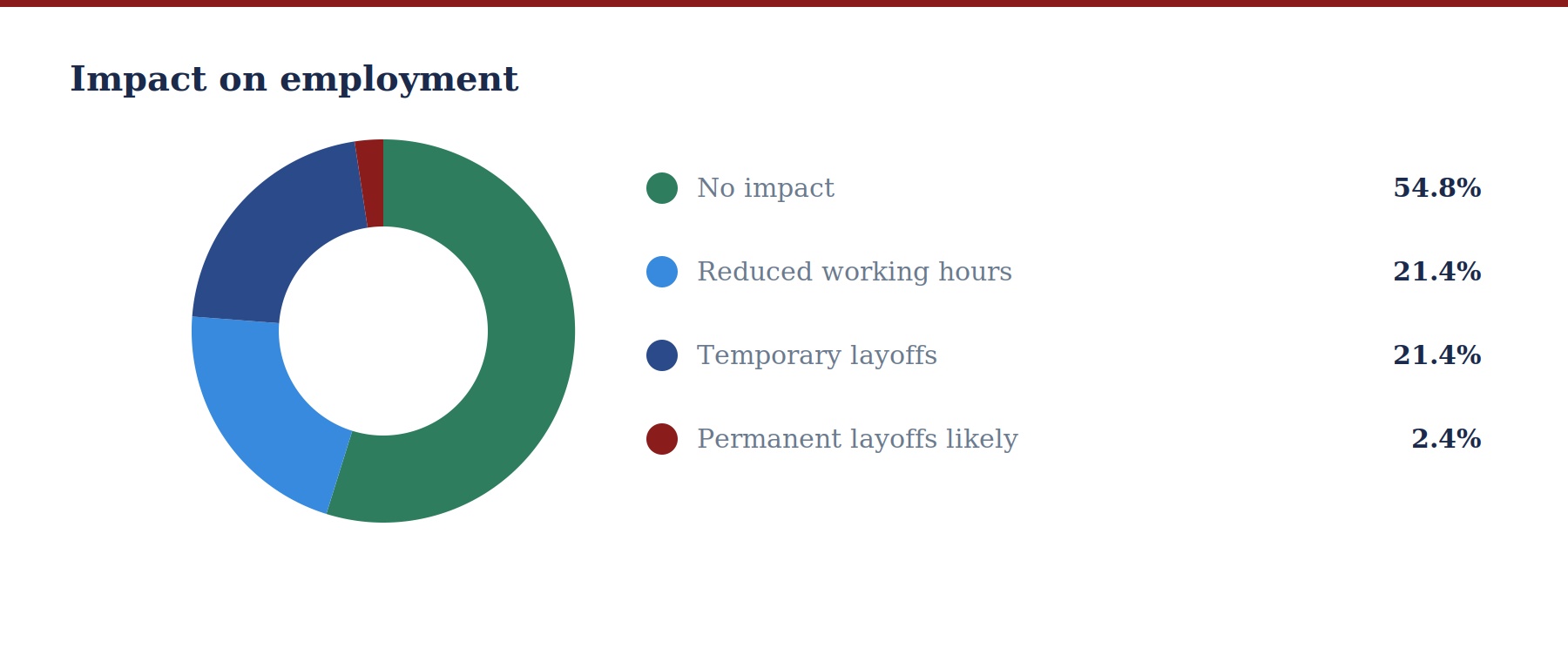

Smaller and solo operators, who lack the reserves to absorb prolonged disruption, face a disproportionate insolvency risk if conditions persist in 2026. Employment impacts are emerging. Forty-three percent of survey respondents report some form of workforce adjustment, reduced working hours, temporary layoffs, or anticipated permanent retrenchment.

Critically, the full employment impact has not yet materialised: a meaningful share of operators describe plans for layoffs, not yet executed. Without intervention, the trajectory is toward a broader labour market shock within the sector.

Operator confidence in the near term is low. Fifty percent of respondents expect conditions to deteriorate further; 29% anticipate only a slow recovery. Only 12% expect a strong rebound in international arrivals over the next three months.

ACUTE STRESS

The survey data, taken together with official arrival statistics, point to a sector under acute and worsening stress. Three immediate priorities emerge clearly from respondent feedback.

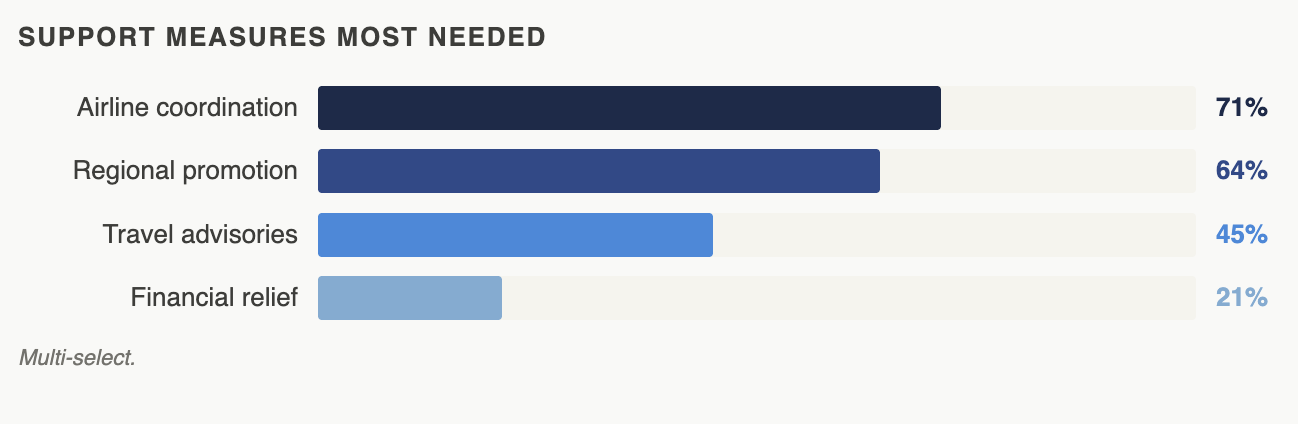

First, airline coordination requires urgent attention. The single most cited support needed is improved coordination with carriers to restore route reliability and explore alternative connectivity, particularly via India and Turkey, before the remainder of the spring season is lost. This is an area where the authorities could play a convening role, engaging airlines and civil aviation bodies to assess what emergency measures are feasible.

Second, targeted promotional efforts toward regional source markets represent a potential near-term buffer. Respondents consistently identified China, India, and Southeast Asia as the markets best positioned to partially offset long-haul losses, given their relative insulation from the conflict's direct effects.

Activating or accelerating promotional campaigns toward these markets is the most consistently requested intervention in the survey data. The extent to which this can compensate for the loss of European and North American visitors in the short term remains uncertain, but the directional case for prioritising these markets is clear.

Third, a clear and consistent travel advisory is overdue. Nepal's geographic distance from the West Asia conflict zone does not appear to be widely understood among affected traveller populations, and the absence of proactive official messaging is likely compounding cancellation rates beyond what the security situation itself warrants.

A unified advisory, clearly distinguishing Nepal from the affected region and affirming the safety of planned itineraries, would address a gap that the private sector cannot fill on its own.

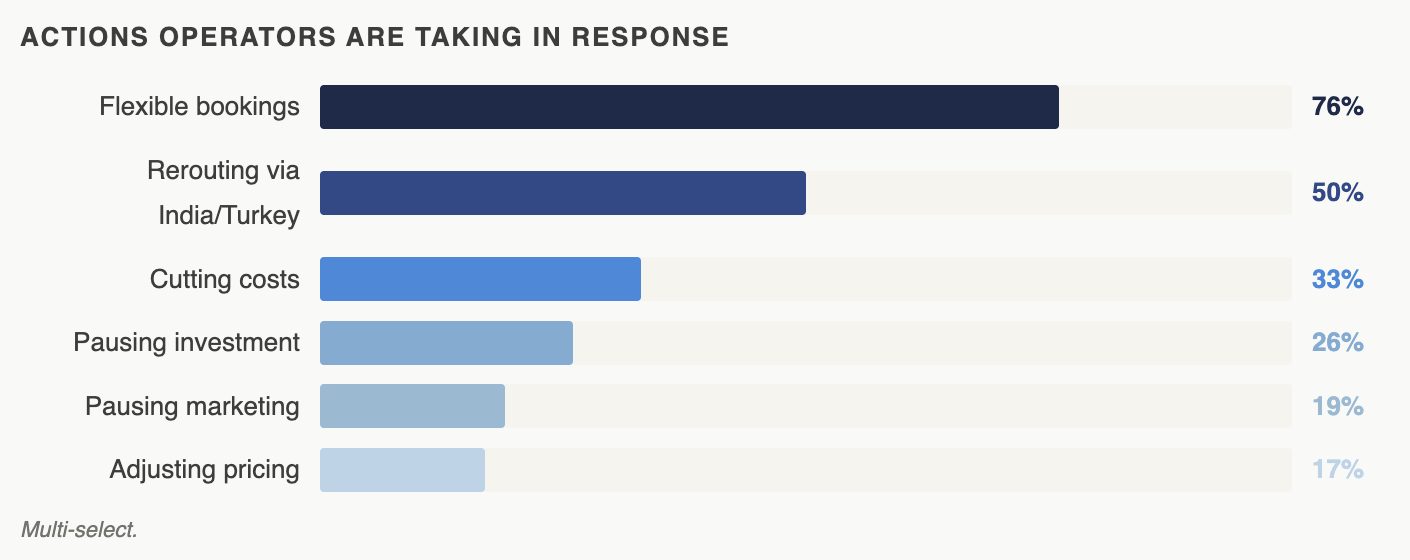

Beyond the immediate term, the financial data points to a liquidity crisis among micro and solo operators. Targeted relief measures, whether in the form of bridge financing, tax deferrals, or fee waivers, warrant exploration before insolvencies accelerate. Similarly, the employment data suggests that a structured monitoring mechanism would allow policymakers to track workforce impacts in near real-time and respond before retrenchment becomes irreversible.

This survey itself illustrates a structural gap: Nepal lacks the real-time data infrastructure needed to detect and respond to tourism shocks with speed and precision. The rapid survey methodology deployed here, designed to capture private sector conditions within days of a crisis onset, should not remain an ad hoc instrument.

Institutionalising open, rapid-response tourism data collection is a precondition for effective crisis governance going forward.

Aanandita Mathema Warmington and Sonia Timalsina are associated with Governance Lab, Nepal Action Research for Tourism Solutions.