Aside from second-guessing what will happen in the restored Parliament on Sunday, the major past-time of urban Nepalis these days is to speculate about the country’s violatile stock market.

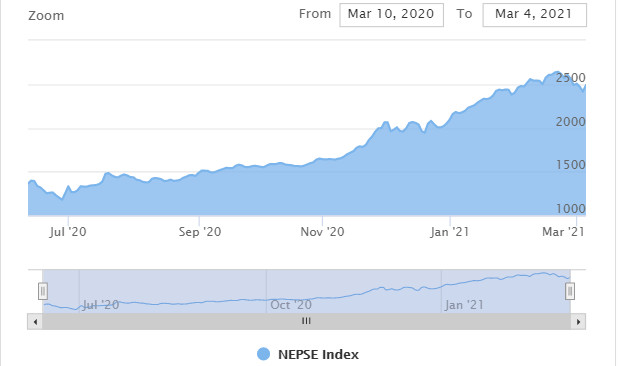

Dring the past six months, the Nepali Stock Market (NEPSE) has soared, which immediately begs the question: is a fall imminent?

The NEPSE Index is at a record high market capitalisation, which is the total value of shares listed in the stock market. Daily turnovers have started crossing the Rs10 billion mark, invetors seem to be raking it in.

All this has happened at a time when the economy is being battered by the impact of the pandemic, which has led to heated debates over whether the market is in a bubble and likely to crash, bringing ordinate ionvestors down with it.

Current highs are the combination of several factors:

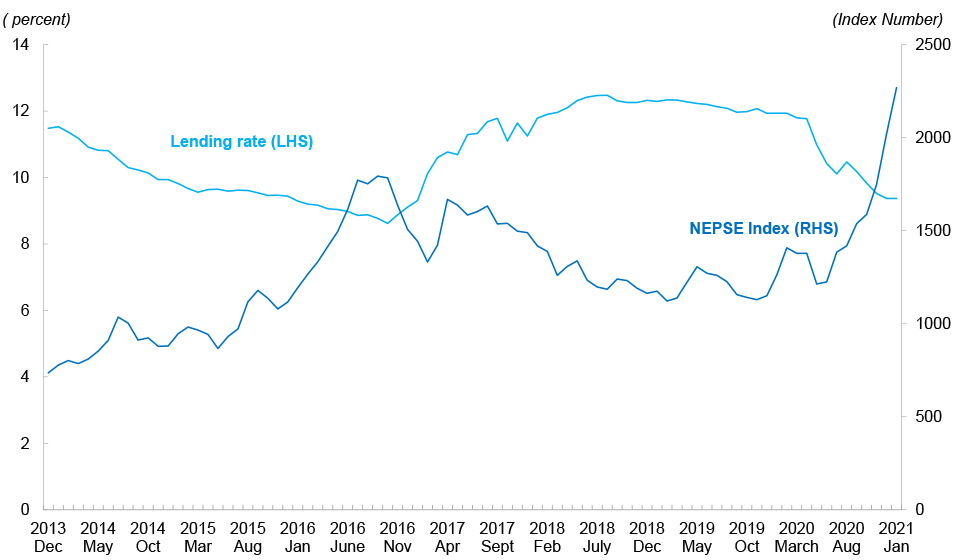

- Low interest rate (see figure 1)

- High liquidity in the banking system

- Dematerialisation (conversion of physical certificates to electronic units) of shares

- Restrictionof ‘kitta-kaat’ in real estate

- Fear of missing out (FOMO)

Low share prices between 2017-2019 have been attributed to the appointment of Yubraj Khatiwada as finance minister. He famously (or infamously for investors) once remarked that investing in stocks was “not productive”.

One factor that has gone relatively unnoticed but has been a game-changer is the advent of ‘online trading’. The possibility to make transactions through the online banking system has ushered in a new breed of investors. Online trading has made the Nepali stock market easily accessible to the public, who can now trade from their living room instead of going to a broker office or bank to make a payment.

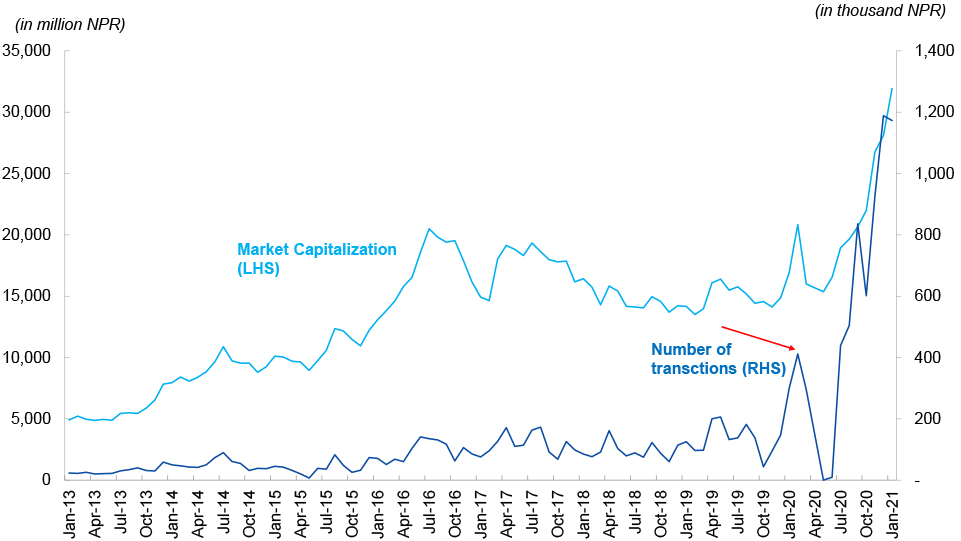

This trend was starting to be reflected in the data before Covid-19 gripped the country (figure 2). From October 2019 to February 2020, the number of monthly share transactions doubled from an average of 200,000 to 400,000, which pushed the NEPSE Index to the 1,600s, despite relatively higher interest rate hovering above 11%.

Following Covid-19 restrictions, the number of transactions further increased and reached a whopping 1.1 million per month in recent months. This reflects the unprecedented entry of retail investors who, with a click of a mouse, can invest money that otherwise would be sitting idle, earning savings account interest rates.

This increased participation and diversification of the investor base is also reflected by the data on stock market penetration. DEMAT accounts have increased from 800,000 in mid-July 2017 to 1.4 million in mid-July 2019, and is currently estimated at 2.5 million -- about 8% of Nepal’s total population.

More than 1.5 million Nepalis applied for the recent IPO of an infrastructure finance company. Compare this number with India, where around 2% of the country’s population invest in the stock market, while in China this number is estimated to be around 7%.

But, online trading also brings a host of new challenges. Asymmetric information, poor advisory services and buying shares based on rumours are big concerns. Investors can lose money in the share market if they overpaid for stock or if their investment horizon is not long enough.

However, by not investing they can also ‘lose’ potential gains. So, investors need to understand and be aware of cognitive biases that limit investing success. It is as much about human psychology as it is about finance and economics.

The importance of diversifying across different companies and sectors, having a long-term investment horizon and personal finance management are even more important these days, but these are severely lacking in Nepal. An investor’s main motto always has to be: buy a diversified set of companies, invest regularly, keep track of the company’s financials and hold for a long period of time.

Crucial reforms now await Nepal’s stock market, these can include:

- Increased participation of companies in manufacturing, agribusiness, etc

- Strong regulation on insider trading

- Better trade settlement systems

- Increasing the limitation of 50 brokers

- Creation of index funds and exchange traded funds (ETFs)

The NEPSE Index jumped more than 100% in the past year. You could argue that its current level is a bit high, but just because it has gone up by 100% it does not mean that it is overvalued, and vice versa.

The cumulative annual growth rate of the NEPSE between 2001 and 2021 is around 12%, which is in line with the 10% return of the S&P 500 (which tracks 500 of the largest US companies) in the same period. During these 20 years, there have also been periods where the NEPSE fell as much as 75% (between August 2008 and June 2011) and soared over 500% (between June 2011 to July 2016).

Stock markets are cyclical by nature. Corrections, and subsequent rises, are bound to happen. In this apparently chaotic environment of ups and downs, one thing is here to stay: a fundamental shift and dynamism thanks to a new breed of investors trading online. This will have short-term disruptions, but it is likely to stabilise the Nepali capital market for years to come.

Santosh Pokharel, CFA works in development sector. Sudyumna Dahal is Doctoral candidate at CAMA, Australian National University.